Like the patriot that I am, I have come to the realization that we really have something going on when it comes to building trains. It’s not just me saying it, some other people have started to take notice….

I started to think about investing in spanish rail manufacturers… I believe we have a strong sector in this country, and I believe climate change and rising oil prices will be good tailwinds.

When it comes to CAGR for the sector, we have to consider it will not just be trains proper, also subways, trams, what have you. And I dont just believe we’re in a position to provide our own trains, I know that we’re in a position to export to Europe, South America, and perhaps others if lucky!

Bullet trains, globally: Bullet Train Market to Reach $77.57 Billion, Globally, by 2031 at 6.27% CAGR: Allied Market Research

Rail, Europe: Europe Rail Infrastructure Market Size to Hit USD 185.04 billion by 2029 | Exhibiting CAGR of 4.52% From 2022-2029

You get the picture…

With that, well, I know we have 2 major train manufacturers that can be invested in to take a look at: CAF, and Talgo.

So, I decided to take a look at CAF.

What do they do?

CAF makes trains, but not just trains, they make trams, metro trains, and not that long ago they purchased Solaris, a manufacturer of hybrid buses, electric buses, trolley buses & trams. Meaning, yes, they make everything transport.

Where do they do it?

The company not only has a presence in Spain but also in Europe (around 50% of their sales are in the continent) and in the rest of the planet. The company seems surprisingly well diversified internationally.

Statements & ratios

In looking at their statements, I dont see much that is remarkable, other than the sale of short term commercial paper on the irish exchange (but this is only me nerding out.)

Their debt, I see as quite normal and nothing to worry about particularly but I did expect them to be able to issue bonds (again, nerd!) instead of having mostly loans.

Something I did notice going back in time is their purchase of Solaris negatively influenced margins (mostly through higher COGS) and they seem not to have recovered much 5 years later.

Another thing to notice is the ROCE (~1.06%) is far from stellar and indicative that indeed perhaps lending money is preferable to building trains currently.

Valuation

I did some exploratory valuation, first of all, and I did not find it very convincing.

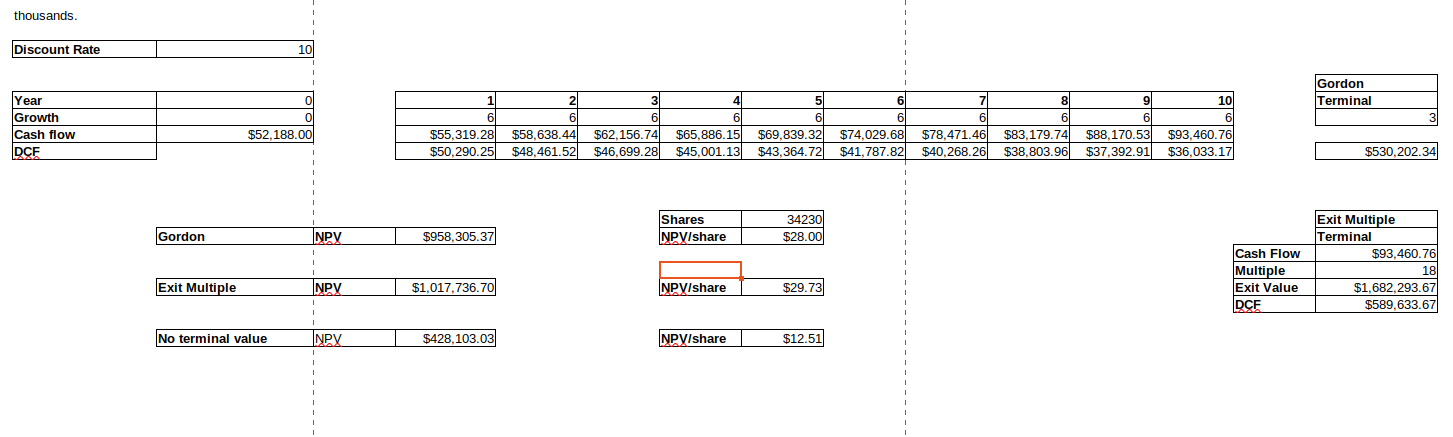

I did a DCF in which I simply punched in the numbers as they seem to be: 6%ish grow, and current profit margins. I used a rather generous 10% discount rate, and the result was that the company seemed fairly priced.

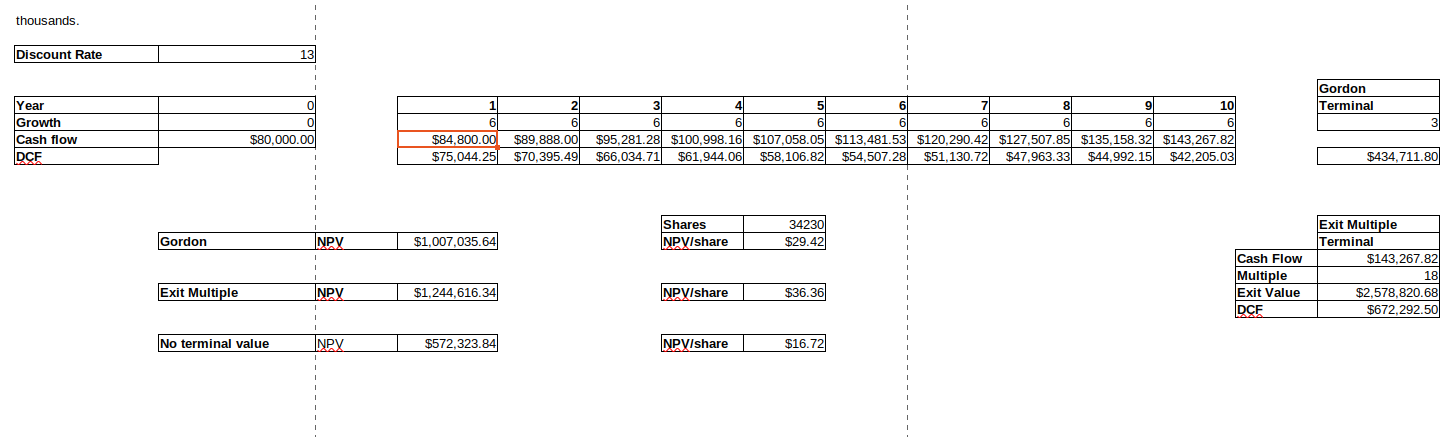

After this experiment, I ran a hypothetical where the margin recovered to 2018 levels, appropriately discounting it at a higher rate, given this is more speculative. The result would be a slight undervaluation, but nothing remarkable.

Conclusion

I like trains, and I like this company. That said, at late april ’23-early may ’23 levels (28 euros ish.), it’s at most a HODL for me.

While you could keep the stock if you own it and possibly wait a little to see if you can realize a slight capital gain, I would not go out of my way to purchase it, as it’s not a bargain, and I don’t see it as stellar enough to purchase at a fair price.

Notes

I don’t own the stock at the time of writing.

Yes, I took a long time to publish as I was busy and didn’t feel this company needed my undivided attention.

Yes, I have cool new DCF spreadsheets, thank you for noticing! 🙂

Leave a Reply