I’ve been meaning to write about this opportunity, but busy, so I’m going to keep it as short and sweet as possible.

I see Cracker Barrel as a cyclical business opportunity trading at a very attractive valuation. Due to how “boring” it sounds, the company is immune to the fad of AI speculative madness which is, truly, phenomenal.

I have kept the accounts around for review for a while now, and other than an intensification of the negative working capital situation, which I would fully expect for this type of business in a downturn, I see nothing wrong here. In fact I see a rather healthy Return On Capital. Indeed, what dreams are made of.

I have read some articles about how CBRL is “uncool” and “needs to appeal to the newer generations”, but, here’s my take: it doesn’t matter at all whether they do or don’t, because the company is worth 2 billion dollars EASILY assuming that it stays FLAT income-wise for the next decade, which is, let’s be fully honest with ourselves, probably a worst case scenario.

Without further adieu:

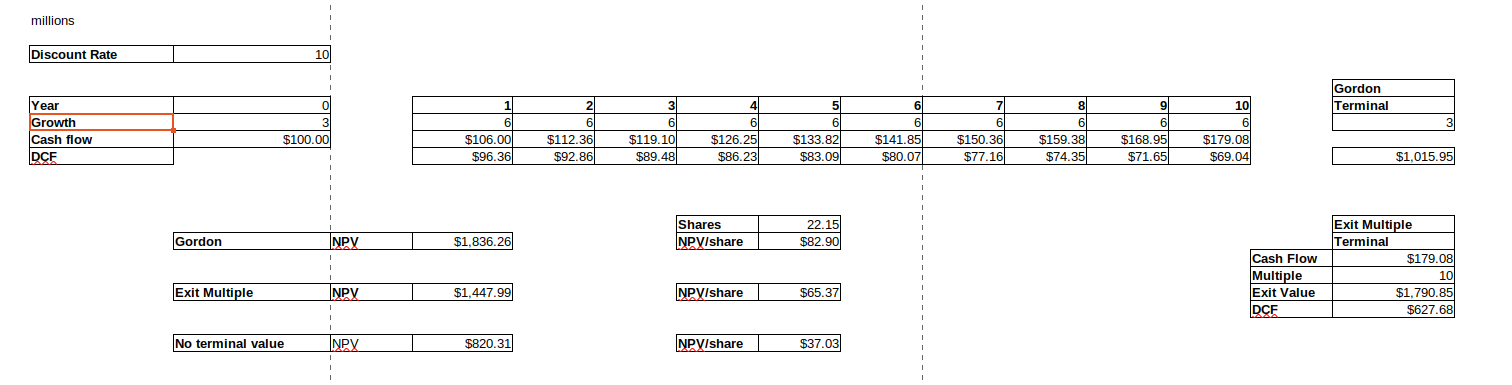

Valuation

The company is very easily worth upwards of 1.8-2 billion USD, because this is assuming such a pessimistic case scenario as to be unreal.

Conclusion

With the company presently trading at 1.4 Billion USD as of writing ($66/share), in my view your only real risk here is not buying enough. It’s a screaming BUY with every positive trait from being very cheap to a good ROCE.

Disclosures

Of course I am a shareholder, Im considering averaging down in fact.

Leave a Reply