It has come to my attention that there is an overwhelmingly negative sentiment going around regarding Amazon, so, intrigued, I decided to see why.

In checking out the latest seekingalpha articles on the matter, I am hit with that unknown unknown: the economy at large. No matter. However, I did notice that it seems like the company hired staff compulsively during the pandemic, that they now must cut. After this bout of exuberance, the company has had a couple bad years. All of this will matter again later in the article. Don’t worry.

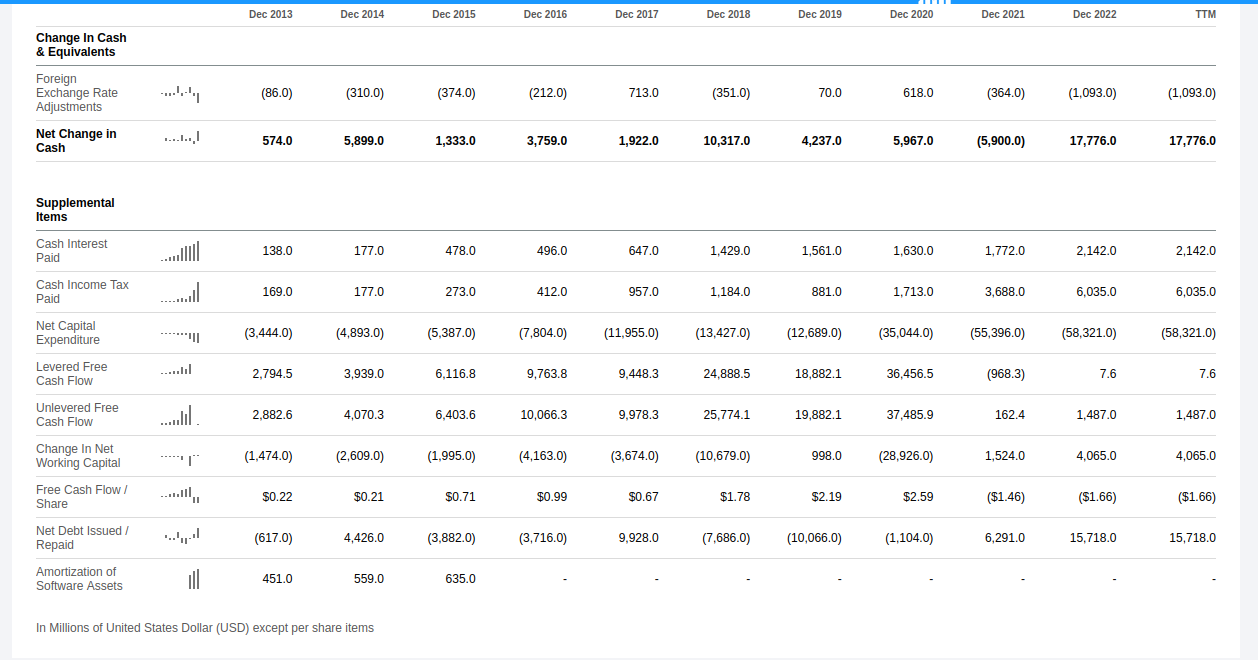

Indeed, things are so bad that Amazon, known for being a cash piling machine seems to be in negative cash flow territory.

Next, I saw that the company seems to have debt (not just commercial paper, or a revolving credit like Facebook back in the day, proper debt) so I decided, seeing how interest rates are doing, that Id be well advised to check that out.

To be fair, some good old horizontal/vertical analysis reveals not much out of the ordinary, the percentage of long term debt seems stable.

The maturities on their debt securities seem decently well spread out, and the interest cost seems reasonable in the current environment. Do consider, however, that financing in the future is likely to be more expensive.

Regarding short term liquidity, the company seems to be doing quite alright even in challenging times with a current ratio of around 1.13.

On to the earnings call.

“We reported overall net income of $278 million in the fourth quarter. While we primarily focus our comments on operating income, I’d point out that this net income includes a pretax valuation loss of $2.3 billion included in nonoperating income from our common stock investment in Rivian Automotive.” Quite interesting. No impact to the core business from this.

Valuation

In valuing Amazon, I will utilize Discounted Cash Flows, as one does.

When it comes to valuation in the current environment, 2 main questions rise to the forefront: That of discount rates and that of “Well, what the hell is an average Amazon year then?” considering the last couple years seem to be particularly dismal, and the prior 2, particularly exuberant.

With regards to the discount rate, I would suggest nothing below 13-15 ish.

With regards to an average year, I reckon it makes sense that your average year without pandemics, or any such nonsense, would net us around 10% in net profit on our sales. Meaning, for the current numbers, around 55 billion dollars in earnings per year. Running my DCF model with this as a base and estimating 20% growth for 5 years, 15% for the next 5, and 3% in perpetuity, I have to discount aggressively to not make this a bargain.

Ill do a last exercise in which I change my growth rate in years 6-10 to 10%, but this is all I need to hear, personally.

Conclusion

Amazon is an excellent business with a significant moat. At the current market capitalization ($100 per share, roughly), it’s undervalued and worth north of $130, most likely north of $150. BUY hand over fist while you can purchase this great business at a good price.

Leave a Reply